The History of Taxes in the U.S.: From No Income Tax to Today's Reality

When the United States was founded, the idea of individual freedom was paramount, and that included freedom from oppressive taxation. Many early Americans were deeply wary of taxes, a sentiment born from their experience with British rule, where "taxation without representation" became a rallying cry for independence. But as we all can see, that has changed. For example, Mainers recently saw a property tax increase of up to 30%, if not more, and another increase to support 'Paid Family & Medical Leave' is just around the corner. How did we get to where we are right now, with the subsequent tax increase just one step away?

Taxes in Early America: A Limited System

Not long after the Founding Fathers wrote the 'Declaration of Independence' on July 4, 1776, and the ending of the Revolutionary War in 1783, "Congress approved a Constitutional Convention to revise the Articles of Confederation: "... the Congress shall have the power to lay and collect taxes, duties, imposts, and excesses, to pay the debts and provide for the common defense and general welfare of the United States." on February 21, 1787, as documented through the Internal Revenue Service (IRS) History Timeline.

On September 2, 1789, Congress established the Department of Treasury. In those days, taxes were generally indirect, meaning they didn't affect citizens directly. The framers of the Constitution designed a system where the federal government relied primarily on customs duties and excise taxes for revenue, believing that taxation should remain minimal and unobtrusive.

While this seemed true for the average working person, some 75 distillers in western Pennsylvania weren't big fans of taxes, which led to the Whiskey Rebellion in 1794. That year "saw the first outright challenge to the U.S. government's revenue laws when a federal court summoned 75 distillers in western Pennsylvania to appear in court and explain why they shouldn't be arrested for whiskey tax evasion. The Whiskey Rebellion set up a clash between citizens and federal officers. The federal government prevailed, but at a cost of $1.5 million to American taxpayers." [Source: IRS History Timeline]

With The War of 1812, also referred to as 'the Second War of Independence,' "Congress passed new internal taxes on refined sugar, carriages, distillers, and auction sales." However, "on December 23, 1817, Congress repealed these and all remaining internal taxes and abolished the position of the Commissioner of the Revenue and all offices to collect them." [Source: IRS History Timeline]

The Introduction of the Income Tax

Then, during the Civil War, the first significant shift occurred. "On July 1, 1862, President Lincoln signed the second revenue measure of the Civil War into law. This law levied internal taxes and established a permanent internal tax system. Congress established the Office of the Commissioner of Internal Revenue under the Department of the Treasury." [Source: IRS History Timeline]

As a temporary measure, an initial income tax was enacted to help finance the Civil War. It was set at 3% on "annual gains, profits or incomes" exceeding $600 and 5% on incomes above $10,000. As one would guess, that wasn't enough even though the income tax raised $20.3 million in the Fiscal Year of 1864. As Sheldon D. Pollack wrote, "Under the 1864 statute, a tax of five percent was imposed on income above the $600 personal exemption, seven and a half percent on income over $5,000, and ten percent on income over $10,000, rather than the $25,000 provided for in the house bill. With this graduated rate structure, the revenue collected under the income tax increased dramatically, reaching nearly $61.0 million in 1865 and exceeding $73.0 million in 1866—the latter constituting one-fifth of total receipts of the federal government for the year."

While the Civil War income tax was meant to be a temporary measure, there was some pushback, as seen by the income tax renewals in 1866, 1867, and 1870, before it finally expired at the end of 1871.

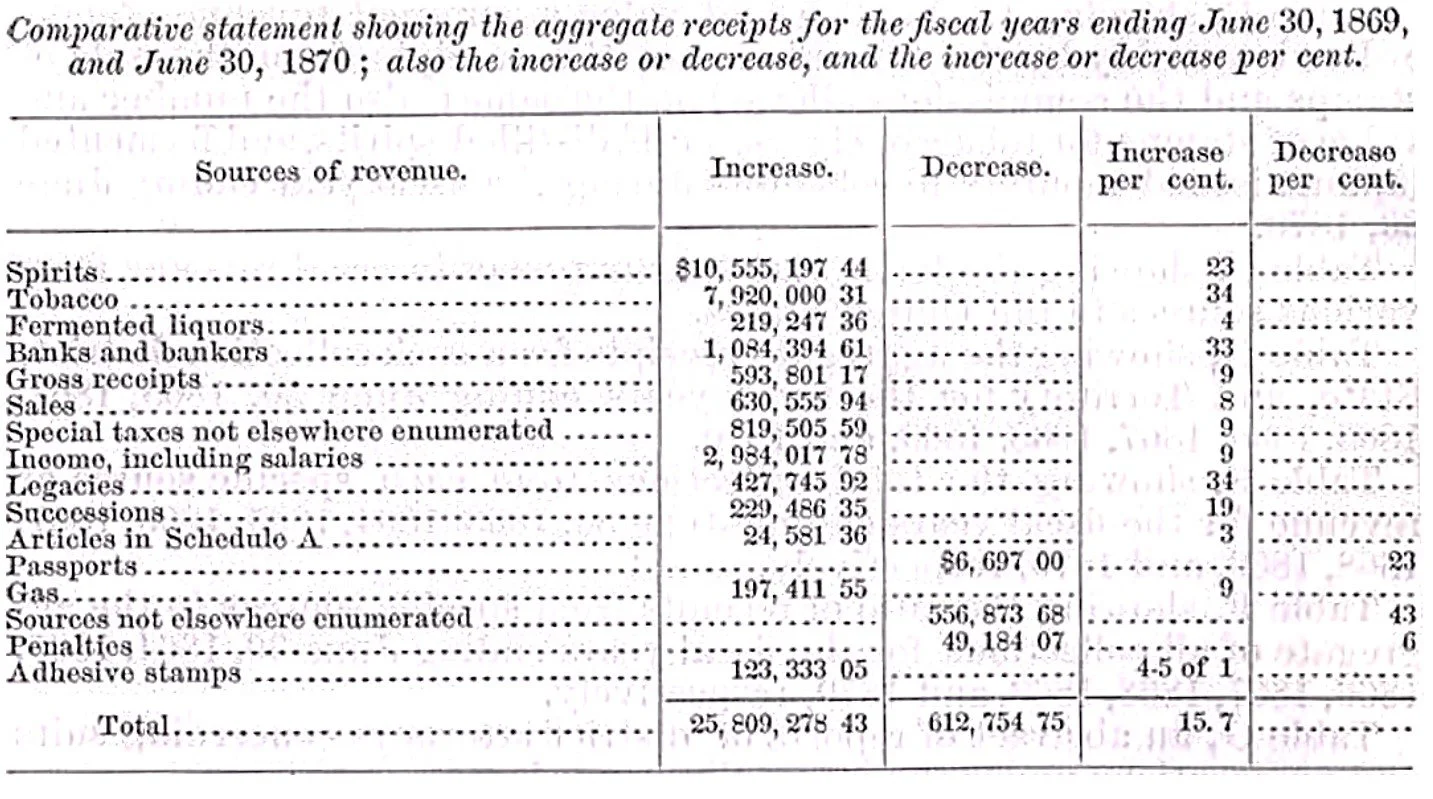

The screenshot below shows an excerpt from the Annual Report of the Commissioner of Internal Revenue from 1870. As you can see, income taxes were the third largest source of revenue in 1869 and 1870.

An excerpt from the Annual Report of the Commissioner of Internal Revenue from 1870

Fast forward to 1913, and the 16th Amendment to the Constitution changed everything.

"The Congress shall have the power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration."

This Amendment gave Congress the constitutional authority to collect income taxes directly without apportioning them among the states. The justification? The government needed stable revenue sources to support a growing nation and its programs. Initially, the tax was designed to affect only the wealthiest Americans, with a modest rate starting at 1%. "Yet in 1913, due to generous exemptions and deductions, less than 1 percent of the population paid income taxes," the National Archives show.

For the history nerds among us: On January 5, 1914, the Treasury Department unveiled the four-page (including instructions) Form 1040, as provided by Public Law 63-16, for the new income tax. In the first year, no money was to be returned with the forms; instead, field agents verified each taxpayer's calculations.

The picture shows Page 1 of the first International Revenue Bureau Form 1040 (from the National Archives, General Records of the Department of the Treasury).

As the U.S. entered World War I, the federal government needed more funding to support its efforts. Sounds oddly familiar, doesn't it? But this time, income tax was no longer a temporary measure. With the Revenue Act of 1916, the lowest income tax rate increased from 1% to 2% while the top rate raised to 15% on taxpayers with incomes above $2 million ($58 million as of October 2023 when accounted for inflation; from 7% on income above $500,000 or $14.5 million when accounted for inflation).

By World War II, income taxes had become a necessity for funding massive military expenditures. As stated by the IRS, "The Roosevelt administration hoped to pay for at least half the cost of World War II by increased taxation. The 1942 Revenue Act sharply increased most existing taxes, introduced the Victory tax (a 5% surcharge on all net income over $624 with a postwar credit), lowered exemptions, and began provisions for medical and dental expenses and investors' expense deductions. Still, taxes only funded 43% of the war's cost, 7% short of the goal."

In 1943, Congress passed the Current Tax Payment Act, which required employers to withhold taxes from employees' wages and remit them quarterly. With that, collecting revenue and spreading the burden across a larger swath of the population became easier. And as we all know, it's not only income tax that the government withholds from an individual's paycheck. There are plenty more, such as the following Federal Taxes: (1) Federal Income Tax, (2) Social Security Tax, and (3) Medicare Tax, State Taxes: (1) State Income Tax and (2) State Disability Insurance, and Local Taxes: (1) Local Income Tax and (2) School District Taxes. Please note that not all taxes apply to everyone, varying state by state. Please refer to your state's revenue or tax department website for detailed information about the taxes withheld.

The transition from a tax targeting the wealthy to one affecting nearly all Americans marked a turning point in how the U.S. government financed its growing responsibilities. This shift also calls for a cultural reevaluation of our perception of taxes and the role of government, in which each of us has a part to play.

But why do taxes keep increasing, and is there a way to stop it? To learn more, please look out for my blog post, "The Expanding Role of Government and the Ever-Increasing Tax Burden."

Resources (links open in a new tab)

Please note that some tax-related resources may only refer to my home state, Maine. Please look up your home state’s specific laws for accurate information.

Maine Gov - Paid Family & Medical Leave – https://www.maine.gov/paidleave/

Maine Gov - Earned Paid Leave - https://www.maine.gov/labor/labor_laws/earnedpaidleave/

Declaration of Independence: A Timeless American Treasure - https://www.dkayinmaine.com/blog-history/blog-us-declaration-of-independence

IRS History Timeline - https://www.irs.gov/pub/newsroom/irs-history-timeline_march-2019.pdf

IRS - Taxes in U.S. History - https://apps.irs.gov/app/understandingTaxes/student/whys_thm02_les05.jsp

US Department of the Treasury - https://www.eatlife.net/us-treasury-building.php

Broxmeyer, J. D. (2014). Politics as a Sphere of Wealth Accumulation: Cases of Gilded Age New York, 1855-1888 - https://academicworks.cuny.edu/cgi/viewcontent.cgi?article=1406&context=gc_etds

When Americans Liked Taxes | Gary Gerstle | The New York Review of Books. https://www.nybooks.com/online/2022/02/23/when-americans-liked-taxes/?printpage=true

Wikipedia – Economic history of the American Civil War - https://en.wikipedia.org/wiki/Economic_history_of_the_American_Civil_War

Sheldon D. Pollack – The First National Income Tax, 1861-1872 - https://udel.edu/~pollack/Downloaded%20SDP%20articles,%20etc/academic%20articles/The%20First%20National%20Income%20Tax%2012-18-2013.pdf

IRS – The Year 1870 - https://www.irs.gov/pub/irs-soi/1870dbfullar.pdf

National Archives – 16th Amendment to the U.S. Constitution - https://www.archives.gov/milestone-documents/16th-amendment

National Archives – First IRS Form 1040 - https://prologue.blogs.archives.gov/2013/04/02/the-16th-amendment-and-100-years-of-federal-income-taxes/

1942 Revenue Act - https://apps.irs.gov/app/understandingTaxes/student/whys_thm02_les05.jsp | https://apps.irs.gov/app/understandingTaxes/teacher/whys_thm02_les05.jsp

Current Tax Payment Act - https://maint.loc.gov/law/help/statutes-at-large/78th-congress/session-1/c78s1ch120.pdf